According to the Bertelsmann Foundation Turkmenistan has an underdeveloped tax system, which is negatively impacted by widespread corruption. The state revenues remain dominated by proceeds from gas exports and the hydrocarbon sector accounts for 80% of the fiscal revenue. In the last 30 years there has not been any detailed and comprehensive analysis of Turkmenistan’s taxation system by international institutions.

The Tax Department under the Ministry of Finance and Economy of Turkmenistan is responsible for tax-related activities. However, its website is not user-friendly and does not provide brief and tailored information on the different types of taxes. Instead, taxpayers have to review the 125 pages long Tax Code to learn about the taxes they need to pay. Neither the Tax Department nor the State Statistics Committee disclose the share of taxes in government revenue. It is also not mentioned in the state budget.

This research examines the current tax system of Turkmenistan and recommends increasing the share of the private sector in the economy as a way to boost the tax revenue without negatively impacting small businesses and low-income families.

What are the tax laws and tax rates in Turkmenistan?

The first tax law in Turkmenistan was signed in January 1992 and it was amended several times. The current Tax Code (“Salgytlar hakynda”) was signed in 2004 and last amended in April 2022. It defines the different types and rates of taxes paid in Turkmenistan:

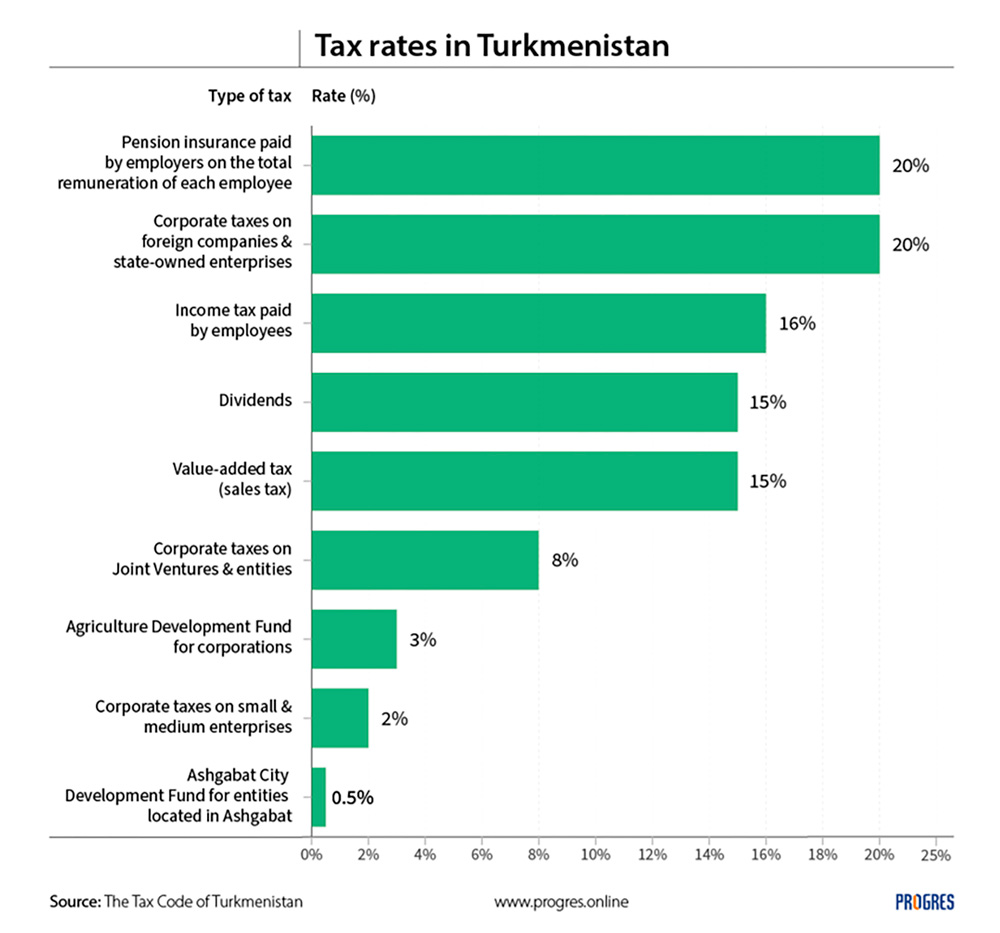

- Employees pay a flat tax rate of 10% on their income along with voluntary 6% social taxes (3% for medical insurance, 2% for pension insurance, and 1% for trade unions). It means every employee working in Turkmenistan pays a fixed tax of 16% irrespective of their income. Income taxes on employees are automatically deducted by their employers on a monthly basis. Employees are not required to file any tax forms. Employees’ payslip summarizes the taxes they have paid.

- Corporations and Joint Ventures pay 8% tax on profit, while foreign companies and state-owned companies (with +50% state ownership) pay 20% taxes on their profit. Businesses need to file their taxes quarterly and biannually.

- Small, and medium-sized enterprises pay 2% tax on their profit. The law does not specify what constitutes a small or medium-sized enterprise.

Turkmenistan uses a flat tax rate on personal income where every employee pays a fixed 10% tax regardless of the amount of their salary. It was first introduced in 2005. All five Central Asian countries as well as Georgia have a flat tax rate system.

The Economist notes that flat tax systems seem to work because they are simple, and easier to administer which helps to reduce tax evasion, enhance compliance, and better integrate the activities in the shadow economy. Authors Adhikari and Alm evaluated the economic effects of the flat tax system in Turkmenistan and have found a positive and significant impact on the country’s GDP per capita, Foreign Direct Investment (FDI) and employment. However, it seemed to have no impact on the country’s domestic investment.

The research paper (“Understanding tax reform in the Central Asian Republics”) written by academics Mokhtari and Ashtari, argues that Turkmenistan has the least capacity and inclination among Central Asian countries to implement the evidence-based tax policy.

How much tax is being collected?

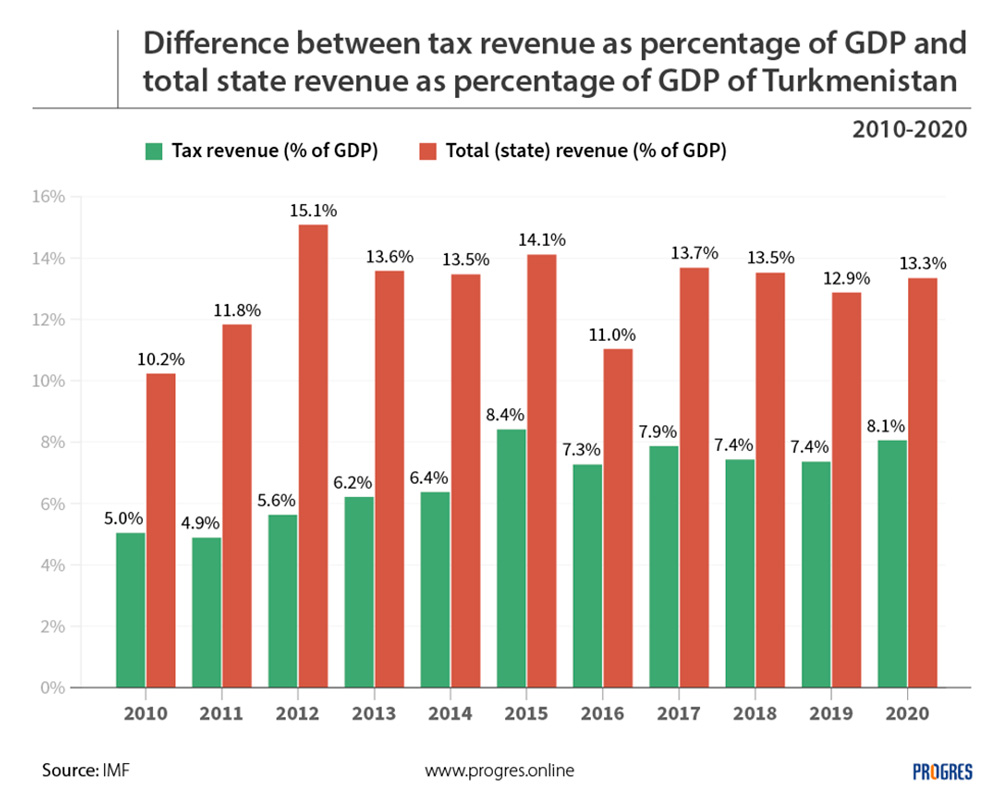

The State Statistics Committee and the Tax Department of Turkmenistan do not report the amount of taxes being collected yearly. According to the IMF, the tax revenue in Turkmenistan in 2020 was 8.06% of GDP while the annual state revenue was 13.34%.

Based on the chart above, there is a large gap between the revenue gained through tax collection and the total government revenue. Taxes account for only a small share of the state revenue while the remaining share might come from revenues made from oil and gas exports.

Turkmenistan has approved the state budget for 2023 calendar year in the amount of 95.1 billion manats (over 27 billion USD per official exchange rate), which is 11.1% higher than the budget for 2022. However, it does not specify the expected share of the revenue from tax collections.

The tax revenue as percentage of GDP is only 8% in Turkmenistan while in other Central Asian countries it is substantially higher. The tax revenue amounted to (IMF):

Donate to support Turkmen analysts, researchers and writers to produce factual, constructive and progressive content in their efforts to educate the public of Turkmenistan.

SUPPORT OUR WORK- 18.74% of the GDP in Uzbekistan (in 2020);

- 18.2% in Tajikistan (in 2019);

- 17.5% in Kyrgyzstan (in 2020);

- 13% of the GDP in Kazakhstan in 2020.

What are the recent developments in the taxation system?

The Ministry of Finance and Economy of Turkmenistan has launched a new public services portal (e.fineconomic.gov.tm) along with a mobile application. The new portal makes it possible to submit documents (statements, applications, and notifications) in accordance with the tax code online without contacting the tax office. The portal is available for legal entities and entrepreneurs to use.

Moreover, as reported by Business Turkmenistan in May 2022, authorities want to update the national tax system and to introduce amendments and additions to the tax code. However, they did not specify which exact changes will be introduced.

How to increase the tax revenue in Turkmenistan?

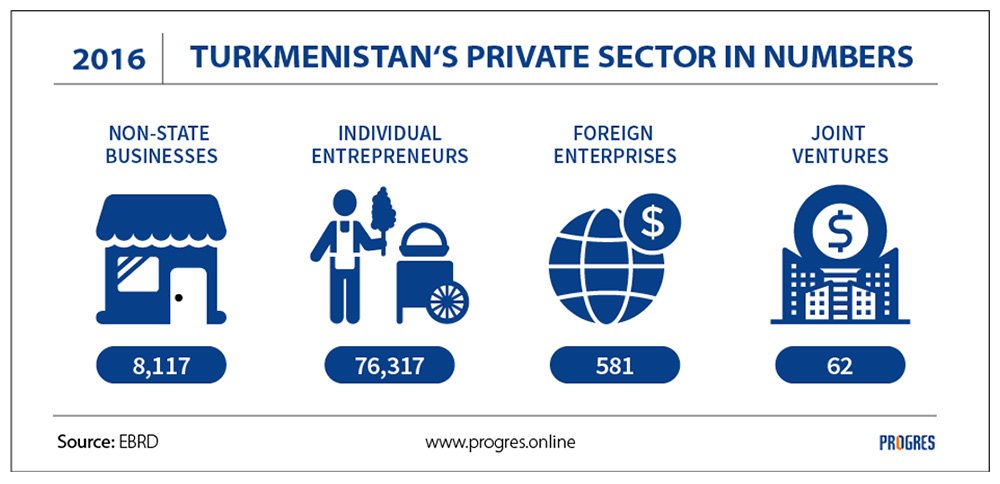

Private enterprises are a major source of tax revenue in many countries. However, the share of the private sector in Turkmenistan’s economy is quite low. According to the EBRD’s country diagnostic report in 2016, nearly 91% of all firms in the country are micro and small enterprises while only 1.1% of firms are large enterprises. In total, there were:

- 8,117 non-state businesses;

- 76,317 individual entrepreneurs;

- 581 foreign enterprises;

- 62 joint ventures.

According to ILO, there were 11,700 registered small enterprises and 55,500 actively working individual entrepreneurs in Turkmenistan in 2005. We can notice that the number of registered enterprises has actually decreased from 2005 to 2016.

For comparison, in Kazakhstan, there were 256,000 domestic non-state enterprises, over one million individual entrepreneurs, and 23,000 foreign companies in 2016. In Uzbekistan, the number of non-state businesses amounted to 239,000. Even adjusted for population size, the number of private firms was 10 times higher in Kazakhstan and 5.5 times higher in Uzbekistan compared to those in Turkmenistan.

When it comes to employment numbers, 279,000 people in total were employed by domestic non-state enterprises, individual entrepreneurs, and foreign companies in 2016 (EBRD). The population of Turkmenistan was close to 6 million in 2016 and the share of the working-age population was 53%, which equals 3.180 million people. Therefore, we can see that for every 1 person in the private sector there were 11 people working in the public sector in 2016.

How greater economic freedom can help increase tax revenue?

Authorities should encourage the creation of more businesses as a means to increase the tax revenue. Heritage Foundation ranks Turkmenistan in 161st place in terms of economic freedom. They also note that the overall freedom to establish and run businesses in the country is very limited. EBRD states that property rights are not properly enforced, which keeps new domestic investments and FDIs away from Turkmenistan. Hence, allowing more economic freedom will enhance the creation of more businesses, which will create new jobs. This will enable the authorities to collect corporate and income taxes from newly created businesses and jobs. With unemployment rates nearing 40%, the creation of new jobs and new taxpayers can raise the tax base without increasing tax rates dramatically.

Additional recommendations to increase tax revenue might include the following:

- Set up an independent advisory board with the representatives of the public and business sectors to develop a plan to modernize the tax system.

- Increase transparency and improve statistics on tax collection. Provide disaggregated data by breaking down the tax collection by each category: personal income tax, corporate tax, pension insurance, etc. Data should be broken down by regions, cities and administrative areas to identify the ones lagging behind and to design appropriate regional development policies.

- Evaluate the impact of tax policies on low-income families. This is especially true for sales taxes and value-added taxes, which are added to goods and services at the point of purchase. For instance, 52.1% of total household expenditures in Turkmenistan constitute expenses on food items (UN Turkmenistan, 2020).

- Institute e-filing to reduce the time, money and effort spent on filing.

- Establish one-stop shops for relevant government services (e.g., for registering businesses and obtaining VAT and company tax numbers).

You can also check out our previous article on the taxation system in Turkmenistan.