The Turkmenistan 2024 Country Profile, published by the World Bank’s Enterprise Analysis Unit, offers a snapshot of the business environment based on interviews with 311 firms conducted between October 2024 and May 2025. The findings reveal a mixed picture: while Turkmenistan demonstrates strong performance in certain operational and infrastructure metrics, the country significantly lags behind in areas such as access to finance, regulatory burden, corruption, and gender inclusion.

Where Turkmenistan Performs Well

Turkmenistan stands out for the speed and reliability of its infrastructure services and annual sales growth, outperforming both regional and income group peers:

- Construction Permits take an average of 32.6 days compared to 90.3 days in Europe & Central Asia and 56.4 days in Upper Middle-Income countries.

- Operating Licenses are obtained in 24.1 days, significantly faster than the regional average (41.2 days).

- Import Licenses require just 7 days, compared to 19.1 days regionally.

- Electrical Connections are established in 10.9 days, much faster than the regional (66.3 days) and income group (49.2 days) averages.

- Water Connections take only 13.4 days, well below regional (38.9 days) norms.

- Power outages reported by only 18.8% of firms in Turkmenistan, significantly fewer than in Europe & Central Asia (26.2%) and Upper Middle-Income countries (43.3%).

- Annual Sales Growth is at 8.4% vs. 5.2% regionally.

Where Turkmenistan Falls Behind

Access to Finance: Access to finance remains a top concern for businesses of all sizes. The banking sector remains underdeveloped, limiting external financing options. Turkmen firms are heavily dependent on internal resources for investment.

- Only 5.8% of firms use bank financing (vs. 28.5% in the region).

- Just 1.1% of investment is financed by banks (compared to 16.2% regionally).

A striking 81.7% of investments are financed internally, significantly above the regional (74.5%) and income group (72.5%) averages.

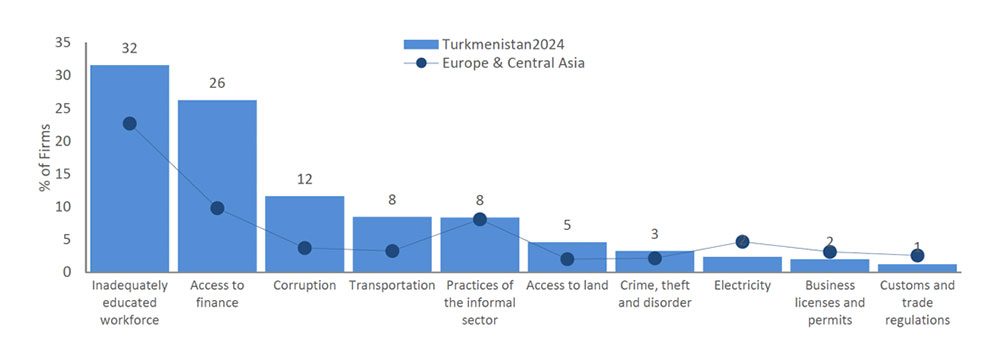

Figure 1. Top Ten Business Environment Constraints

Corruption and Bribery: Corruption remains a major concern, particularly in obtaining permits and dealing with tax authorities, but its severity varies significantly by region.

- Bribery incidence is high:

- 10.6% of firms experienced at least one bribe payment request, significantly above the Europe & Central Asia average (6.1%).

- Gift-giving to officials is common:

- 13.4% of firms reported giving gifts for construction permits (vs. 6.7% regionally).

- 9.6% gave gifts during tax meetings (vs. 5.4%).

- 6.8% for import licenses (vs. 3.4%).

- 4.3% for operating licenses (vs. 3.2%).

- 17.2% of firms said they had to offer gifts simply “to get things done”, nearly triple the regional average of 6.3%.

- Bribery depth (the share of public transactions involving informal payments) in Turkmenistan is 9.2%, nearly double the regional average of 5%.

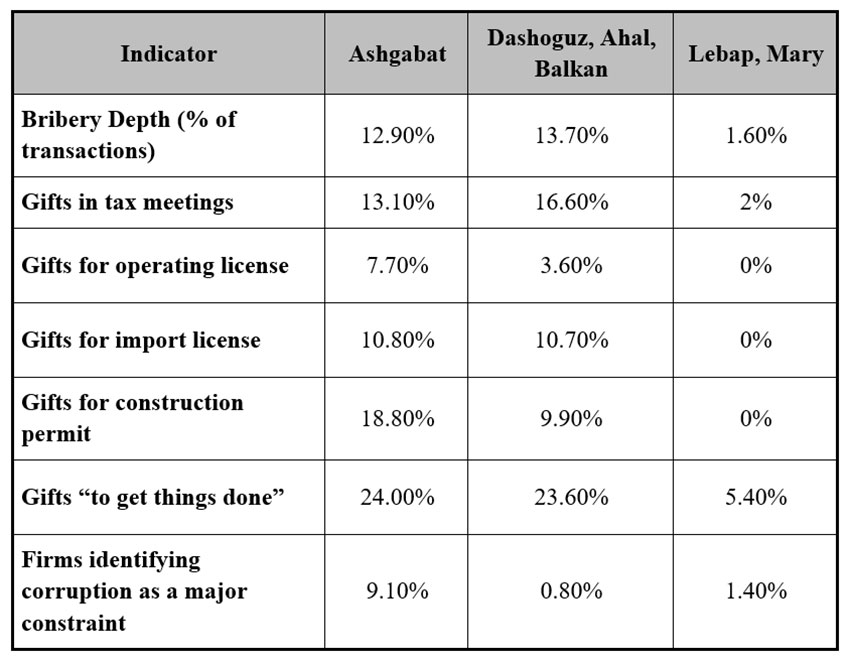

The contrast is stark in Ashgabat and western regions (Dashoguz, Ahal, Balkan), bribery is far more prevalent. In Lebap and Mary, rates are significantly lower – raising questions about either real regional differences, underreporting, or local administrative practices.

Donate to support Turkmen analysts, researchers and writers to produce factual, constructive and progressive content in their efforts to educate the public of Turkmenistan.

SUPPORT OUR WORKFigure 2. Regional Variations in Reported Levels of Corruption

Despite this evidence, only 4.7% of firms nationally see corruption as a major constraint, a surprisingly low figure compared to the regional average of 14.7% and the global figure of 23.4%. This mismatch suggests – normalization of bribery in business processes, fear of retaliation for reporting corruption or low trust in institutional mechanisms for redress.

Workforce Skills and Training:

- Only 26.5% of firms offer formal training to employees, below both regional (36.2%) and income group (33.8%) averages.

- The proportion of skilled workers in production roles is 63.1%, below the regional norm (81.6%).

Gender Inclusion: The low participation of women in ownership and leadership points to untapped economic potential and structural gender gaps.

- Mere 10.4% of firms with women participation in ownership and 5.9% of firms with majority women ownership, which is significantly lower than the regional average, 34.4% and 12.9%, respectively.

- Only 6.1% of firms have a female top manager, compared to 17.3% in Europe & Central Asia.

- 12% of firms owned or managed by women were among those that held a government contract in the last 3 years compared to 38.2% regional average.

- 28.3% of full-time workers are women vs. 35.9% in the region.

Foreign Investment:

- No surveyed firms reported at least 10% foreign ownership – 0%, compared to 8% in both Europe & Central Asia and Upper Middle Income countries – highlighting a lack of foreign direct investment engagement.

Regulatory Burden and “Time Tax”: The burden of bureaucracy – manifested through high time costs and frequent tax inspections – discourages business growth and increases informal interactions, and potentially creates room for corruption.

- Senior management spends 13.5% of their time dealing with government regulations, well above regional (8.0%) and income group (9.6%) levels.

- 59.3% of firms had to meet with tax officials, double the regional rate (29.2%).

Customs Delays:

- Export clearance averages 8.7 days and import clearance 10.8 days, slower than regional averages (4.6 and 6.2 days respectively), though closer to Upper Middle-Income norms.

According to the World Bank, Turkmenistan’s private sector benefits from efficient infrastructure services and promising firm-level growth in sales and employment. However, broader structural reforms are needed to unlock its full economic potential. Improving access to finance, reducing regulatory burdens, strengthening anti-corruption measures, and promoting gender equity in the business environment will be essential to fostering sustainable private sector development.