The IMF Working Paper “Recognizing Reality: Unification of Official and Parallel Market Exchange Rates” (Simon T. Gray, 2021) discusses the benefits of unifying overvalued official exchange rates with parallel market rates. Drawing on the experiences of Uzbekistan, Azerbaijan, and Kazakhstan among others, the study highlights the importance of aligning exchange rates with market realities to promote economic stability and growth.

Countries maintaining an overvalued official exchange rate often face difficulty in meeting legitimate demand for foreign exchange (FX). When restrictions are imposed on FX, it usually results in a parallel FX market. Case studies from the past 10 years, where countries have unified their exchange rates, indicate that such a move is unlikely to cause a sharp rise in inflation. This is because prices in the real economy often already align with the parallel market exchange rate.

For Turkmenistan, which faces similar issues with maintaining an overvalued exchange rate and the existence of the parallel market which is 457% more expensive, the experiences of Uzbekistan, Azerbaijan, and Kazakhstan offer a way forward.

Uzbekistan

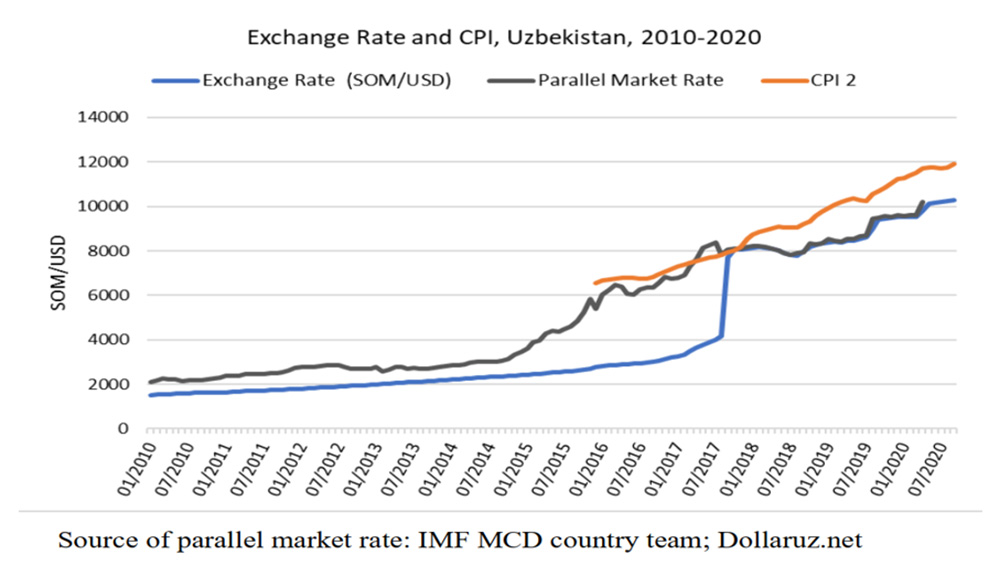

In Uzbekistan, the large depreciation of the Uzbek som in 2017 brought the official rate in line with the parallel market by depreciating the exchange rate by 86%. This move did not lead to significant inflationary pressure because, prior to the unification, prices already reflected the parallel market rate. The peak inflation was 20.1% in the first year following the unification.

Policy interest rates were tightened from 9% to 14% to manage inflation. Following the unification, the official and parallel market rates have moved in sync, suggesting that the transition to a market-clearing rate was well managed and beneficial for stabilizing the economy.

Azerbaijan

Donate to support Turkmen analysts, researchers and writers to produce factual, constructive and progressive content in their efforts to educate the public of Turkmenistan.

SUPPORT OUR WORKAzerbaijan underwent two adjustments to its exchange rate. The first devaluation of 24.5% was not sufficient to achieve a market-clearing rate. However, following a significant 62.4% of devaluation in December 2015, the country adopted a new pegged exchange rate. This allowed for the stabilization of inflation, which peaked at 14.5% after the devaluation but returned to single digits within two years. The sharp increase in interest rates from 3% to 15% during this period, alongside fiscal adjustments, helped stabilize both inflation and the exchange rate.

Kazakhstan

Kazakhstan faced two rounds of devaluation. The first, in early 2014, did not fully correct the overvalued exchange rate. However, after another substantial devaluation of 95.8% in 2015, monetary policy responded with a sharp rise in interest rates to 17%, helping to mitigate inflationary pressures. Despite the depreciation of the Kazakhstani tenge, inflation remained relatively contained with a peak inflation of 17.4% within the first year following the unification.

Lessons for Turkmenistan

Turkmenistan faces similar issues with maintaining an overvalued exchange rate and the existence of the parallel market which is 457% more expensive, the experiences of Uzbekistan, Azerbaijan, and Kazakhstan offer a way forward. Like its neighbors, Turkmenistan could benefit from unifying its exchange rates at a level that reflects real market conditions. This can reduce distortions in the economy, promote investment, and stabilize inflation over time.

- Monetary Policy Adjustments: A key component of the successful transitions in these countries was the tightening of interest rates to control inflation after the devaluation. Turkmenistan would need to adopt a similar approach, ensuring that its monetary policy supports a stable currency post-unification.

- Supportive Fiscal Policy: Fiscal adjustments, such as reducing deficits and avoiding excessive government spending are essential to maintaining confidence in the currency.

- Communication and Transparency: Clear communication with the public and the business community is critical during the transition to a unified exchange rate. This minimizes uncertainty and speculation, which could otherwise exacerbate inflationary pressures.

The study concludes that unifying the exchange rates at a market-clearing level is crucial for long-term economic health, particularly for countries suffering from prolonged exchange rate distortions. Moving to a market-clearing exchange rate can stimulate economic development, provided it is backed by sound fiscal and monetary policies. However, addressing the underlying causes of exchange rate imbalances, such as unsustainable fiscal deficits or weak monetary policies, is critical. Without these supporting elements, merely adjusting the exchange rate will not stabilize the economy in the long term.